Yes No Share to Facebook

Calculating Above the Guide Line Increases

Extraordinary Municipal Tax Increases

Last Updated: July 02 2026

Question: How do you calculate an Ontario above-guideline rent increase when municipal taxes and charges rose extraordinarily?

Answer: If you are a landlord in Ontario and you need to calculate an Above-Guideline Rent Increase (AGI) due to extraordinary municipal tax increases, a Paralegal from Cross Legal Services can help you work through the eligibility and the math under the Residential Tenancies Act, 2006 and O. Reg. 516/06 (including how to determine the threshold using the guideline plus 50 per cent, then how to compute the allowance using the Base Year, Reference Year, and the applicable factor). In practical terms, you confirm your First Effective Date, confirm your Base Year and Reference Year tax amounts, test whether the municipal increase is “extraordinary” under the regulation, then use the L5 calculation steps to estimate the allowable rent increase you can apply to tenants across Ontario, and you can book a free consultation by calling (289) 443-0675.

Calculating Above-Guideline Rent Increases

Part One: Extraordinary Municipal Tax Increases

In Ontario, residential landlords can apply for an above guideline rent increase (AGI) if they are faced with extraordinary increases in municipal taxes and charges. This is a step-by-step guide of the calculation process for such increases under O. Reg 516/06, Section 29, and an explanation of, crucial definitions of terms that are foundational to understanding eligibility and calculation methods.

In Ontario, residential landlords can apply for an above guideline rent increase (AGI) if they are faced with extraordinary increases in municipal taxes and charges. This is a step-by-step guide of the calculation process for such increases under O. Reg 516/06, Section 29, and an explanation of, crucial definitions of terms that are foundational to understanding eligibility and calculation methods.

Legal Basis

Residential Tenancies Act, 2006 (RTA) - Section 126 states that a landlord may apply for an AGI due to extraordinary increases in the costs of municipal taxes and charges.

What is considered extraordinary and how that is calculated and applied is set out within O. Reg 516/06, Sections 21, 28 and 29

21.(1) The factor to be applied for the purposes of paragraph 6 ofsubsection 29 (2) and paragraph 2 ofsubsection 30 (2) is determined by dividing the total rents of the rental units in the residential complex that are subject to the application and are affected by the operating cost by the total rents of the rental units in the residential complex that are affected by the operating cost.

(2) For the purpose of subsection (1), the rent for a rental unit that is vacant or that is otherwise not rented shall be deemed to be the average rent charged for the rental units in the residential complex.

28. (1) An increase in the cost for municipal taxes and charges is extraordinary if it is greater than the guideline plus 50 per cent of the guideline.

(2) For the purposes of subsection (1), the guideline is the guideline for the calendar year in which the effective date of the first intended rent increase referred to in the application falls.

(3) Despite subsection (1), if the guideline is less than zero, any increase in the cost for municipal taxes and charges is deemed to be extraordinary.

Rules

29. (1) The rules set out in this section apply to the Board in making findings related to extraordinary increases in the cost for municipal taxes and charges.

(2) The amount of the allowance for an extraordinary increase in the cost for municipal taxes and charges is calculated as follows:

1. If section 28 applies in respect of the increase, adjust the reference year costs for municipal taxes and charges by the guideline plus 50 per cent of the guideline determined in accordance with subsection 28 (2).

…

5. Subtract the reference year costs for municipal taxes and charges, as adjusted under paragraph 1, from the base year costs for municipal taxes and charges, as adjusted under paragraphs 2, 3 and 4.

6. Multiply the amount determined in paragraph 5 by the factor determined under section 21.

(5) Despite section 28, if the guideline is less than zero per cent, for the purposes of the calculations in subsection (2), the guideline is deemed to be zero per cent.

(6) An increase in municipal taxes and charges as a result of an appeal of a tax assessment shall not be considered under subsection (2) if the application for the rent increase was filed more than 12 months after the decision on the appeal was issued.

Key definitions:

Base Year (BY) The "Base Year" is defined as the most recent calendar year completed at least 90 days before the date the first effective date (FED) the intended rent increase takes effect. This timing ensures the rent increase reflects accurate and comprehensive data that encompasses one complete year.

Example: For a rent increase effective on July 1, 2025, the base year would be the calendar year that ended on December 31, 2024.

Reference Year (RY) The "Reference Year" is the calendar year immediately preceding the base year, serving as a benchmark for comparative analysis of cost changes.

Example: If the base year is 2023, then the reference year would be 2022.

First Effective Date (FED) The first date that the rental increase begins.

Step 1: Verify Eligibility for AGI

Before making any calculations, it’s critical to determine whether the increase in municipal taxes qualifies as "extraordinary" (s 28(1)). In the example below, I created a sample set of criteria to illustrate the steps and calculations. For simplicity I have not added any adjustments for tax assessment appeals or late issued tax notices discussed under sections 29(2)2,3 and 4.

Sample Scenario:

| Guideline Increase for the Year: | 2.5% |

| 50% of Guideline: | 1.25% |

| Base Year Taxes Paid: | $10,000.00 |

| Reference Year Taxes Paid: | $9,000.00 |

A: Determine Threshold

Before calculating the actual increases in municipal taxes, it is essential to establish the threshold that defines an extraordinary increase.

The threshold for an extraordinary increase is determined by adding the guideline increase for the year plus 50% of that guideline. This total percentage sets the minimum increase in municipal taxes that must be exceeded to qualify for an AGI. The guideline rate used in this calculation is the guideline rate set by the Ontario government for the year in which the FED of the rent increase occurs.

For example, if the FED is in 2025 then use the rate for that year. In our Sample Scenario, with a guideline increase of 2.5%, the threshold is calculated as follows:

Calculation to Determine Threshold

Threshold = 2.5% = 1.25% = 3.75%

B: Verify Eligibility for AGI

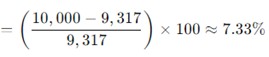

Once the threshold is established, verify your eligibility by calculating the actual increase in municipal taxes from the reference year to the base year.

Calculation to Determine Eligibility:

Calculate the Percentage Increase in Municipal Taxes by using the following formula:

Which in our scenario would be:

C: Check against Threshold

| Calculated Increase: | 7.33% |

| Threshold for Extraordinary Increase: | 3.75% |

Since the calculated increase of 7.33% exceeds the threshold of 3.75%, the increase qualifies as extraordinary, making the AGI application eligible under this criterion.

Step 2: Calculation of AGI

Once an extraordinary increase has been determined the next step is to apply the rules as set out in s. 29. This is where the wording in the Regulations, the instruction sheets, and guidelines become difficult to follow. I have attempted top break it down step by step. Again, I have left out any late notice adjustments or additional assessment charges for simplicity.

Our example scenario:

| Guideline Increase: | 2.5% |

| Base Year (BY) Costs for Municipal Taxes and Charges: | $10,000.00 |

| Reference Year (RY) Costs for Municipal Taxes and Charges: | $9,500 |

| Additional charges from tax assessment appeals: | none |

| Late-issued tax notices: | none |

| Monthly Rent per Unit: | $3,000.00 |

| Number of Units: (Assume unit for simplicity) | 1 |

| Annual Rent Collected: ($3,000 per month x 12) | $36,000.00 |

| Section 21 Factor:(all units are equally affected ) | 1:1 |

A: Adjust Reference Year Costs

First, adjust the reference year costs by the guideline increase plus 50% of that guideline. Simply put, you have to add to the Reference Year the amount that would be included in the threshold rate.

The Board considers the Guideline Increase plus the 50% of the guideline that makes up the Threshold Rate (in our case 3.75%) an ‘ordinary’ increase. What we are doing here is adding the ‘ordinary’ portion of the increase to the Reference Year to determine what amount is ‘ordinary’.

| Guideline Increase: | 2.5% |

| 50% of Guideline: | 1.25% |

| Total Adjustment Percentage: | 3.75% |

Calculation for Adjusted Reference Year Costs:

Adjusted RY Costs = RY + ( Threshold rate x RY )

For our calculations:

Adjusted RY Costs = $9,500 + (3.75% x $9,500) = $9,500 + $356.25 = $9,856.25

B: Determine Extraordinary Increase

Next, compare the adjusted reference year costs (Step A above) to the base year costs to determine if there's an extraordinary increase.

Here they are saying subtract the adjusted reference year costs from the base year and the amount that is left over is the extraordinary increase.

| Base Year Costs: | $10,000.00 |

| Adjusted Reference Year Costs: | $9,856.25 |

Net Increase = BY – Adjusted RY

For our calculations:

Net Increase = $10,000 - $9,856.25 = $143.75

C: Apply Section 21 Factor

In the context of section 21 of O. Reg. 516/06, the factor ensures that operating cost increases are proportionally distributed among the rental units in the residential complex. If all units are equally affected by the cost increase, the factor will result in an even distribution, with each unit bearing an equal share of the increase. For example, if there are two residential rental units, and both are equally affected by an increase of $100, each unit would bear $50 of the increase. This simplifies the calculation, as the total increase can be directly divided among the units without further adjustment.

If a portion of the rental complex is commercial and not residential then the commercial portion of the complex would be removed from the calculations by applying this factor.

Calculation with Section 21 Factor:

Rent Increase per Unit = $143.75 x 1 = $143.75

Step 4: Calculate the Percentage Increase

From the previous calculation, we determined that the total allowable rent increase due to extraordinary increases in municipal taxes is $143.75 for the year. We will now convert this into the total allowable increase into a percentage of the total annual rent collected and apply this to determine the monthly rent increase per unit:

| Total Allowable Rent Increase: | $143.75 |

| Total Annual Rent Collected: | $36,000.00 |

| Monthly Rent per Unit: | $3,000.00 |

Calculation for Percentage Increase:

For our scenario that would be:

Step 5: Apply the Percentage to Monthly Rent

Finally, we apply this percentage increase to the monthly rent to determine the actual monthly rent increase per unit.

Calculation for Monthly Rent Increase:

For our scenario that would be:

Overview and Outcome:

Under this scenario, with all units affected equally by the tax increase, each unit in the complex would see a monthly rent increase of about $12 due to the extraordinary increase in municipal taxes. This method ensures that the rent increase is proportional to the overall rent revenue of the property and is fairly distributed among all tenants based on the rent they pay.

- Percentage Increase: The calculation from Step 4 provides a percentage increase of 0.399%, which represents the proportion of the total annual rent that the extraordinary tax increase constitutes.

- Monthly Rent Increase: Applying this percentage to the monthly rent (as calculated in Step 5) gives a rent increase of approximately $12 per month per unit.

Conclusion

The process of completing an L5 Application for an above the guideline rent increase due to extraordinary municipal tax increases is designed to be straightforward and accessible for landlords.

- Hearings related to these applications are conducted in writing, not in person, which can significantly reduce costs associated with attending hearings and streamline the process.

- Most of the calculations required for the application are standardized, and the form itself guides landlords through what specific inputs and documentation need to be submitted. This means that much of the complex financial computation is simplified, requiring landlords to input only a few key figures and attach the necessary documentation.

Permanent Increase and Timing Considerations:

- Once in a 12 Month Period: It is important to remember you can only lawfully raise the rent once within a twelve-month period.

- First Effective Date (FED): For an increase paid in 2024, considering the application process and timing, the First Effective Date of the rent increase would typically be April 1, 2025. This scheduling accounts for the necessary notice period to tenants and the end of the base year (2024) during which the increase occurred.

- Anticipate Long Wait Periods: The Landlord and Tenant Board (LTB) often experiences significant backlogs, resulting in prolonged wait times for hearing dates and final decisions. Given these potential delays, it is advisable for landlords to submit their applications early. An early application not only ensures that the process can commence without undue delay but also helps in planning for the effective management of rental units and tenant relations during the interim period.

Key Takeaway

The application fee is currently set at $233, which may initially seem substantial, especially if the calculated rent increase for the current year appears modest. However, it is important to recognize that the increase, once approved, becomes a permanent adjustment to the rental base rate and subsequent guideline increases will be based on this new base rate.. This permanency underscores the value of proceeding with the application despite the upfront costs. Applying for and securing this increase is the only formal method to adjust the rent base legally and permanently, ensuring that the rent structure reflects the real costs incurred due to changes in municipal taxes.

Additional Resources:

To simplify the process further and ensure accuracy in your calculations, I offer a free 1/2 Hour consultation to discuss your needs and review your calculations. Please call to book a time.

Guideline 14 : Applications for Rent Increases Above the Guideline

NOTE: A significant quantity of online searches featuring “lawyers near me” or “best lawyer in” typically indicates an urgent requirement for competent legal assistance rather than a particular designation. In Ontario, licensed paralegals are governed by the same Law Society that regulates lawyers and possess the authority to represent clients in specified litigation matters. Advocacy, legal analysis, and procedural proficiencies are integral to this function. Cross Legal Services provides legal representation within its licensed parameters, focusing on strategic positioning, evidence preparation, and compelling advocacy aimed at securing effective and beneficial outcomes for clients.